Syllabus: GS3/Economy

Context

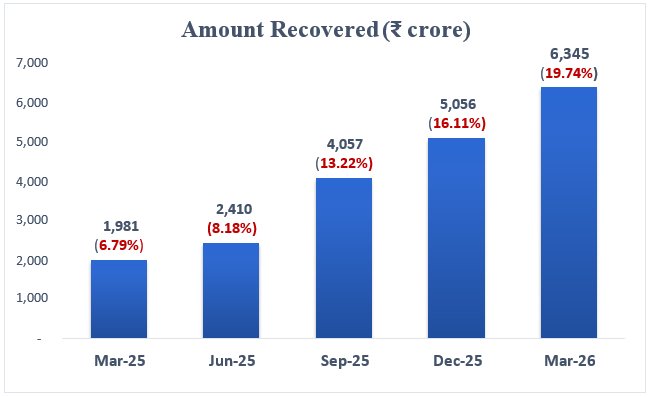

- National Asset Reconstruction Company Limited (NARCL) strengthens India’s Stressed Asset Resolution Framework, and accelerates recoveries in FY 2025–26.

Evolution of India’s Stressed Asset Resolution Framework

- Early Mechanisms: Debt Recovery Tribunals (DRTs), 1993; SARFAESI Act, 2002; and Asset Reconstruction Companies (ARCs).

- However, these mechanisms suffered from delays, low recovery rates, and coordination issues.

- Structural Reform: Insolvency and Bankruptcy Code (IBC), 2016: It introduced a time-bound insolvency resolution process; shifted control from promoters to creditors; and improved recovery rates and credit discipline.

- It created a ‘creditor-in-control model’ and marked a paradigm shift in India’s resolution ecosystem.

- Asset Quality Review (AQR) By RBI & Banking Reforms: These improved transparency in NPAs; and resulted in recapitalisation of banks strengthened balance sheets.

- Need for a ‘Bad Bank’ Model: Despite IBC success, large, complex NPAs remained unresolved, multiple lenders led to coordination failures; and ARCs faced capital constraints.

- It led to the creation of a centralized ‘bad bank’ structure.

- Bad banks help by aggregating stressed assets, enabling professional resolution, and improving price discovery.

National Asset Reconstruction Company Limited (NARCL)

- Institutional Structure: Government-backed ARC (‘bad bank’), that works with India Debt Resolution Company Ltd. (IDRCL) focusing on large-value stressed assets.

- Key Functions: Acquisition of stressed assets from banks; aggregation of exposures across lenders; and resolution via IBC process, market-based sale, and restructuring mechanisms.

Role in the Resolution Ecosystem

- Balance Sheet Cleansing: Removes legacy NPAs from bank books and enhances credit capacity of banks.

- Value Maximisation: Consolidation improves bargaining power, and professional management enhances recovery outcomes.

- Complementing IBC: IBC is a legal resolution framework; and NARCL is an institutional execution mechanism.

- NARCL reduces coordination failures and delays inherent in multi-creditor systems.

Performance and Emerging Trends

- NARCL has accelerated recovery momentum in recent years, focusing on large-ticket NPAs improves systemic efficiency.

- It helps in the development of a secondary market for stressed assets.

- Target acquisition: ₹2 lakh crore stressed assets; continued focus on large-value resolutions; and strengthening of secondary market for distressed assets.

- NARCL is expected to play a pivotal role in enhancing financial sector resilience, supporting India’s credit growth cycle; and enabling efficient capital allocation.

Role in Strengthening Banking Sector

- Balance Sheet Cleansing: NARCL enables banks to transfer legacy NPAs, improve asset quality, and focus on fresh lending.

- It aligns with RBI’s emphasis on capital adequacy and credit flow.

- Capital Recycling: Recovery of stressed assets releases locked capital; and facilitates credit expansion in productive sectors.

- Improved Recovery Ecosystem: Works alongside IBC, DRTs, and SARFAESI Act; and reduces delays and coordination issues among multiple lenders.

Challenges in the Framework

- Legal and Procedural Delays: IBC timelines often breached due to litigation.

- Valuation Issues: Difficulty in pricing distressed assets.

- Moral Hazard: Banks may rely excessively on transfers to NARCL.

- Capacity Constraints: Need for deeper distressed asset markets and investors.

Way Forward

- Strengthen IBC infrastructure and judicial capacity

- Improve secondary market liquidity for stressed assets

- Enhance transparency in asset valuation

- Promote private sector participation

- Integrate technology and data analytics in resolution.

Previous article

Between Polling and Counting, How EVMs are Stored in Strongroom

Next article

Recalibrating Food Systems to Hydrological Realities